A Curious Threshold

(or: An Open Letter to the Esteemed Underwriters of Global Risk...aka all the scumbag insurance companies insuring ships transiting the Strait of Hormuz, but abandoning U.S. families after disasters)

To whom this most certainly concerns,

I recognize and respect disciplined underwriting. That said, I am attempting to better understand the threshold at which a risk transitions from “cautious” to “acceptable,” particularly given your collective role in supporting insurance capacity for maritime transit through active geopolitical chokepoints.

It is a curious threshold.

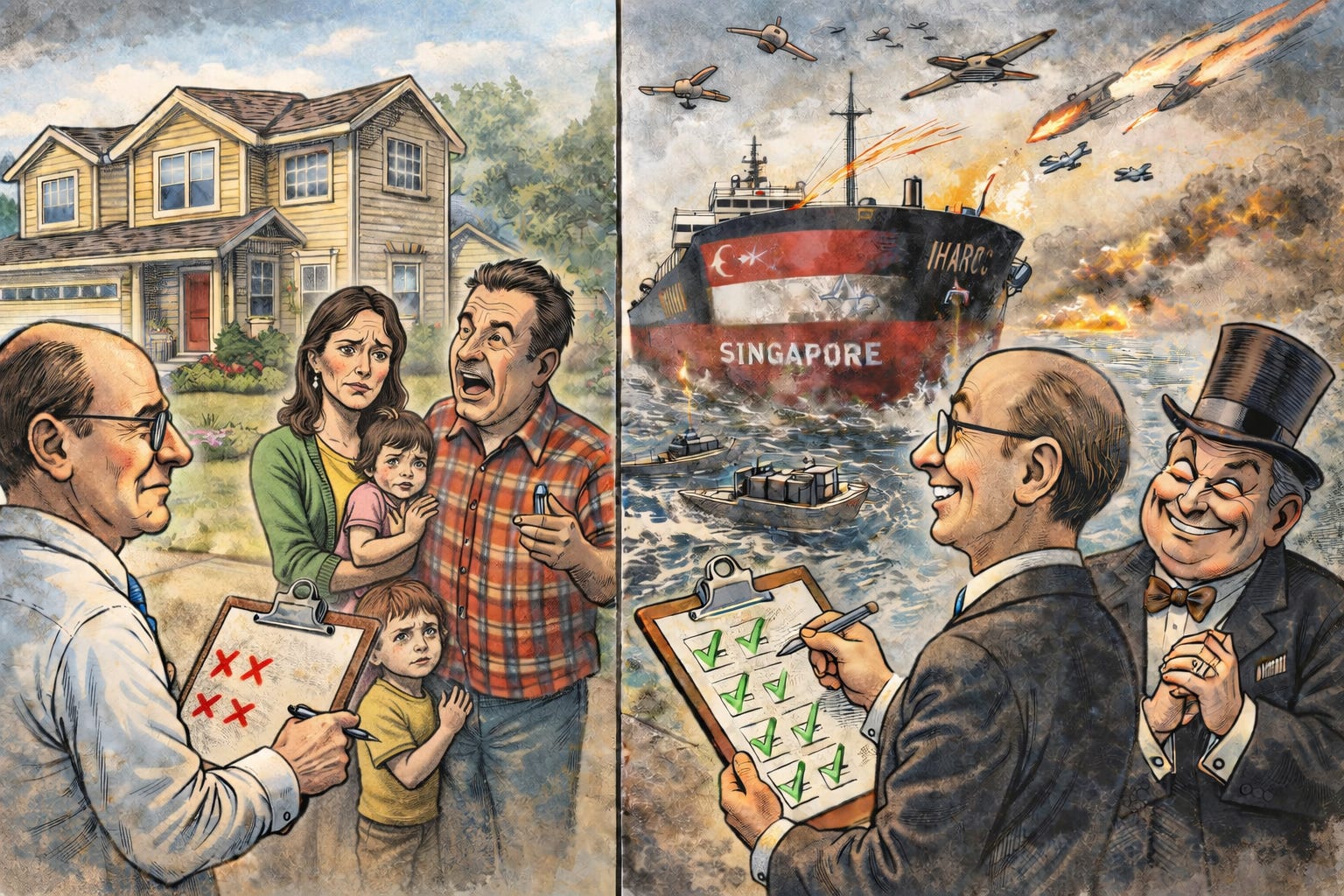

A vessel navigating the Strait of Hormuz, a corridor currently contested by Iran, the United States, and Israel, where missiles, drones, and airstrikes are not theoretical but are actual ongoing features of that very kinetic environment, is, with sufficient premium, a perfectly acceptable risk.

We are speaking here of a waterway where missile systems have already been employed, where drones probe and detonate, where naval forces posture and reposition, where traffic has at times collapsed under what amounts to a functional blockade, and where the sky above is not merely dramatic but actively contested. Fighter jets conduct strikes. Radar lights up. Advisories are written in the language of escalation.

And still, coverage proceeds.

Policies are written. Terms are adjusted. Risk, having been properly introduced to a price, becomes civilized.

Meanwhile, a single-family home in Pacific Palisades, fixed to its foundation, engaged primarily in the quiet activities of existing, perhaps watering a few plants beneath an otherwise unremarkable sky, finds itself just beyond the frontier of insurability.

I begin to suspect that the distinction lies not in the severity of the risk, but in who gets to own the aftermath.

Some risks are not merely insured, they are escorted. They pass through corridors where capital is already seated comfortably, where losses can be priced, distributed, and absorbed without disturbing the arrangement of who holds the deed when the accounting is done. These risks, though dramatic, are cooperative. They threaten movement, not ownership.

Other risks are less accommodating. They do not inconvenience the system so much as they inconvenience the people inside it. They concentrate loss in the hands of individuals first, and only later translate into opportunity for those with the patience and liquidity to collect what remains.

It would seem your collective discipline is reserved for these.

Where risk endangers the flow of capital, it is stabilized, insured, and ushered safely along its route. Where risk merely dislodges people from what they own, it is allowed to proceed with a certain philosophical detachment.

The sequence is familiar.

Insurance withdraws. Financing tightens. Prices soften.

Then, quite miraculously, capital returns, refreshed, selective, and ready to purchase what it previously found too dangerous to protect.

I hesitate to call it a strategy. It has all the elegance of one, without the inconvenience of being declared.

The wealth does not disappear. It simply changes address.

There is, of course, a practical distinction that clarifies matters.

Insuring ships and their cargo preserves the smooth functioning of commerce, which in turn preserves the comfort of those who sit nearest its flow. When a shipping lane tightens, so too do the well puckered buttholes of banking and shipping and insurance magnates from here to timbucktu. The sphincter of concern constricts violently as the effects of the disruption travel upward, where decisions are ultimately made and relief is promptly arranged.

Insuring homes after a disaster operates…differently. The benefit disperses outward, quietly and expensively, among people whose misfortune does not threaten to interrupt a balance sheet so much as it inconveniences a conscience.

When risk threatens systems, it is met with urgency and accommodation.

When it threatens individuals, it is met with caution and explanation.

There is another consequence worth noting, though it is rarely advertised.

When insurance becomes scarce, ownership grows fragile. A house that cannot be insured cannot be financed, and a house that cannot be financed begins, quite naturally, to look less like an asset and more like a liability.

At that point, the market develops a sudden and curious efficiency.

Those who must sell do so under pressure. Those who can buy do so without it.

Capital, which had previously declined to assume the risk at a reasonable price, reappears at a discount to acquire the asset itself. What could not be insured becomes, in due course, worth owning, provided one is sufficiently well-positioned to wait out the hazard.

It is an elegant arrangement.

Risk is socialized at the moment of loss, privatized at the moment of opportunity, and the transfer is conducted with all the quiet dignity of a market correction.

I ask only for clarity.

At what precise point does a risk become respectable enough to insure? When does “cautious” yield to “acceptable”? And is it possible, with sufficient documentation and cooperation, for a stationary residence to achieve the composure of a vessel in a contested strait?

I remain willing to assist in this transformation.

To that end, I am prepared to make several adjustments to better align my property with your (apparently) preferred risk profile:

I can arrange for intermittent aerial disturbances, perhaps a scheduled overflight or two, to lend the sky a more credible sense of participation.

I am open to installing a modest radar array in the driveway, should it improve detectability and therefore insurability.

If required, I can coordinate periodic alerts of “heightened tension” or even “kinetic escalation”with my neighbors to ensure that the most appropriate and insurable atmosphere is maintained.

I would even consider renaming the cul-de-sac a “strategic economic corridor,” if such designation improves underwriting confidence.

In short, I am prepared to make the risk more legible, more theatrical, and, of course more respectable. Also, to be absolutely certain my property is congruent with your policies, I have enclosed a totally unrelated donation to AIPAC.

The house does not move. It does not escalate. It does not require escort.

But it is willing to learn.

Should my property acquire missiles, I trust you will reconsider promptly.

Sincerely,

Mr. John A. Policyholderseverywhere…

-

P.S. For clarity, the pattern described above is not isolated but structural, spanning retail carriers such as State Farm, Allstate, Farmers Insurance, and Travelers, whose underwriting is shaped upstream by reinsurers including Munich Re and Swiss Re; meanwhile, assets in materially higher-risk environments (ie heavily contested warzones) remain insurable through distributed markets like Lloyd’s of London and specialty underwriters such as Beazley and Hiscox, all ultimately capitalized and influenced by large asset managers including BlackRock and Blackstone, with residual exposure redirected into mechanisms like the California FAIR Plan; the outcome, consistently, is that risks threatening capital flow are insured and protected and preserved and distributed, while those concentrated at the level of individual ownership are allowed to accumulate until they resolve into acquisition opportunities for big money.

Note: the situation is so tenuous that the fragile little cease-fire has already been shook up by Israeli shenanigans less than 24 hours after it began…(what else is new?!)… and not to mention an additional bit of weirdness that whatever toll is gonna be required to ships passing the street now is gonna be due in cryptocurrency…(can anybody say bibicoin or trumpcoin)?